Just like in California, Colorado recently passed a bill to create a statewide insurance plan to write insurance policies in high risk areas. Why are most major insurers now leaving California? What does this mean for the future of property insurance in Colorado? Why are insurance rates in Colorado skyrocketing? What is the new “tax” on certain Colorado property owners? Will Colorado homeowners still be able to get private property insurance? How does Colorado’s fair insurance plan impact rates and policy holders?

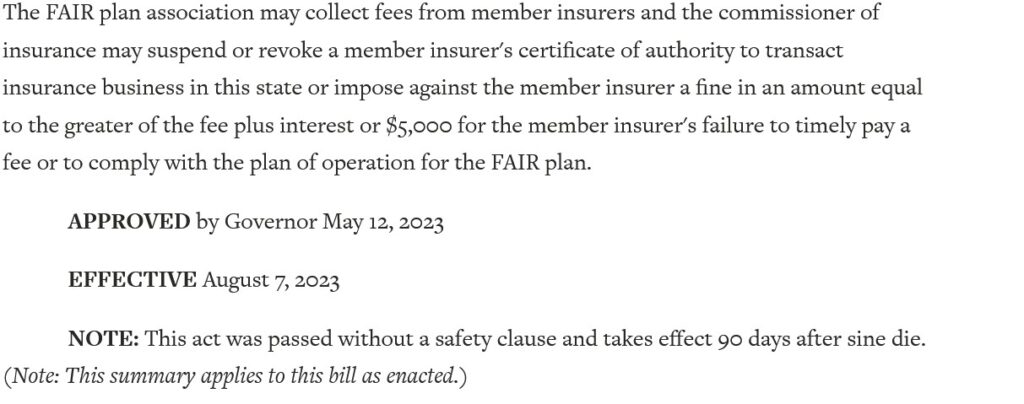

The Fair act HB 23-1288

First, you have to love the names that the legislature gives to the various acts, unfortunately the fair act is anything but fair to most property owners as it is basically a transfer tax from low-risk policy holders to high risk property holders. Furthermore, it requires anyone writing insurance in Colorado to pay into the new “pool”. The new law is in all senses a new tax on a select group of property owners. This bill was signed into law by Governor Polis and now filtering through the insurance marketplace. Below are more details.

Colorado following in the footsteps of California’s insurance debacle

Just like California, Colorado is now getting into the insurance market. HB23-1288: State Sponsored property insurance plan which is now law. This is a bill looking for a solution. State-run or state-created insurers of last resort started cropping up in the 1960s in coastal and urban areas where property owners faced high risks — from fires and hurricanes — and couldn’t get traditional coverage from private insurance companies, said Mark Friedlander, a spokesman for the Insurance Information Institute, another insurance industry trade group.

Theoretically, the new state run policy would insure property owners in extremely high risk areas that are not able to obtain fire insurance. As a lender in Colorado for over 20 years I have not seen a single instance where insurance was not attainable at a price. The reason that the issue of not being able to get insurance is even coming up is that insurance providers are drastically raising rates in high risk areas due to huge losses in the last several years from wildfires.

I’ve been dropped on my properties due to “high fire risk” and live and have lived in the mountains and foothills throughout Colorado. Every time I was dropped I was able to obtain insurance albeit at a price and with certain stipulations (tree removal, defensible space, etc…)

What is in the Colorado Property insurance plan:

The law creates an unincorporated public entity, the fair access to insurance requirements plan association (association), to help persons who are unable to find coverage in the voluntary market obtain provide property insurance coverage for their real property when such coverage is not available from admitted companies.

The Fair Plan must:

- Establish, offer, and maintain a property insurance and a commercial property insurance policy that satisfies the requirements specified in the bill;

- Establish a reinsurance association; and

- Assess and share among member insurers all expenses, income, and losses based on each member insurer’s written premium in the state.

The association is managed by a board of directors consisting of 9 members appointed by the governor. The board is required to administer the fair access to insurance requirements plan (FAIR plan).

The FAIR plan must include rates that:

- Are not excessive, inadequate, or unfairly discriminatory;

- Are actuarially sound so that revenue generated from premiums is adequate to pay for expected losses, expenses, and taxes and the cost of reinsurance; and

- Reflect the investment income of the FAIR plan; and

- Reflect the cost of reinsurance or to other capital risk transfer markets.

What is happening in California’s insurance marketplace:

State Farm General Insurance Co. said it’s no longer accepting new applications for property and casualty coverage in California last week, a year after Allstate Corp. also paused new policies, worsening what FAIR Plan, a state-mandated insurance pool, called a “looming insurance unavailability crisis.”

“We have a lot of people going naked, which means they have no insurance,” said Bill Dodd, a Democrat state senator representing fire-scarred Napa County and other parts of Northern California. “What my constituents want is insurance.”

The FAIR Plan, which offers minimal coverage and high rates is meant to be a provider of last resort, but enrollments have surged 70% since 2019 to 272,846 homes in 2022.

Colorado will have a similar outcome to California

Over the next 3-5 years, you will see major insurance companies no longer willing to write policies in higher risk areas. We are already seeing the beginning of this with many insurance companies no longer willing to write policies in the foothills and many mountain communities. California is a cautionary tale that was not heeded in Colorado.

The real reason for many carriers dropping coverage in Colorado is cost vs expense. Rates must be considerably higher in higher risk areas to compensate for the risk of loss. In California State Farm requested a 28% increase in rates to compensate for the higher risk and expenses for writing policies in higher risk areas. California prohibited the increase and State Farm pulled out of the market.

Taxpayers subsidizing high risk properties and areas

By creating a state run insurance carrier, all property owners are subsidizing high risk properties. Even after the huge fires a few years ago, there have not been material changes to prevent a similar incident again. For example, wood fending is still allowed even though wood fences contributed to losses in the last fire season due to the fire “climbing” the fence to the house. Furthermore spacing was also highlighted as a concern as the fire could easily jump from one house to another due to their close proximity.

In essence, we are building very similarly, and the state of Colorado thinks the outcome will be different. Furthermore, counties continue to allow building in extremely high-risk areas which at the end of the day will be at every Colorado property owners expense.

Property values drop when property insurance is dropped or rising exponentially

Porter said First Street Foundation’s research in California concluded that “the moment that an individual gets a non-renewal letter from the private insurance market, they essentially lose 12% of their property value.” I actually think that a 12% drop could be optimistic as it becomes increasingly difficult if not impossible to get financing as a lender would require property insurance.

We are seeing this trend play out in Colorado with some foothills properties have difficulties selling due to insurance issues (extremely high prices, or inability to get insurance. For example, I saw a recent house that was valued around 400k go from insurance of 3k/year to 14k a year. At this price point, a typical borrower cannot absorb over 1k/month escrow for insurance and the price of the property must fall substantially.

This is just the beginning as this past year in our servicing portfolio our annual increase in property insurance premiums is around 30%. These huge jumps are not sustainable and driving the cost of ownership up exponentially

Summary:

Colorado’s proposed plan to get into the insurance business is a bad solution to a problem that is not real. The overwhelming majority of property owners can obtain insurance at a price. The real reason that the state is getting involved in the insurance business is because property owners do not like the price of the new coverage. Remember, the price reflects the risk that insurance companies have and creates incentives and disincentives in the market. For example, when I renewed my insurance after getting dropped, the new carrier required certain items (removal of trees, protected space, etc…) to get insurance. Without making these changes, I would have paid a substantially higher price.

This is a terrible idea to create a state-run property insurance fund to subsidize properties in high-risk areas. A better solution would be to address the root causes of the issues including building in extremely high-risk areas and building requirements like no wood fencing after what happened in the Marshall fire. Unfortunately, the legislature is misguided in their proposal for a state run insurance program and at the end of the day everyone in the state will pay substantially more to subsidize others as opposed to making structural reforms.

It is unfortunate that this bill does not address the root cause of losses which is building in very high-risk areas. To help HB23-1288 could have made a simple change that it will not insure any houses built after 2022, but instead these bills further pass on the costs to all property owners in Colorado to subsidize high risk properties. A state-run insurance carrier is an idea that has already played out in other states and will lead to unintended consequences including higher prices, less insurance options, and ultimately a taxpayer bailout of the state insurance plan. We are already seeing this play out in California and Florida.

Additional Reading/Resources:

- https://www.bloomberg.com/news/articles/2023-06-02/buying-a-home-in-california-is-already-hard-state-farm-s-exit-makes-it-harder?srnd=premium

- https://leg.colorado.gov/bills/hb23-1174

- https://leg.colorado.gov/bills/hb23-1288

- https://www.cnbc.com/2024/02/05/what-homeowners-need-to-know-as-insurers-leave-high-risk-climate-areas.html

We are a Colorado Private/ Hard Money Lender funding in cash!

If you were forwarded this message, please subscribe to our newsletter

I need your help! Do not worry, I’m not asking you to wire money to your long-lost cousin that is going to give you a million dollars if you just send them your bank account! I do need your help though, please like and share our articles on linked in, twitter, facebook, and other social media and forward to your friends/associates I would greatly appreciate it.

Written by Glen Weinberg, Owner Fairview Commercial Lending. Glen has been published as an expert in hard money lending, real estate valuation, financing, and various other real estate topics in Bloomberg, Businessweek ,the Colorado Real Estate Journal, National Association of Realtors Magazine, The Real Deal real estate news, the CO Biz Magazine, The Denver Post, The Scotsman mortgage broker guide, Mortgage Professional America and various other national publications.

Glen resides in Colorado, lends in Colorado, owns property in Colorado, and services loans in Colorado which provides a unique real estate prospective of what is actually happening on the ground both in Denver and throughout Colorado. My goal from this blog is to provide an honest assessment of what I see happening in Colorado real estate and how it will impact real estate owners, buyers, realtors, mortgage professionals, etc…

Fairview is the recognized leader in Colorado Hard Money and Colorado private lending focusing on residential investment properties and commercial properties both in Denver and throughout the state. We are the Colorado experts having closed thousands of loans throughout the Front range, Western slope, resort communities, and everywhere in between. We also live, work, and play in the mountains throughout Colorado and understand the intricacies of each market.

When you call you will speak directly to the decision makers and get an honest answer quickly. We are recognized in the industry as the leader in Colorado hard money lending with no upfront fees or any other games. Learn more about Hard Money Lending through our free Hard Money Guide. To get started on a loan all we need is our simple one page application (no upfront fees or other games)

Tags: Denver hard money, Denver Colorado hard money lender, Colorado hard money, Colorado private lender, Denver private lender, Colorado ski lender, Colorado real estate trends, Colorado real estate prices, Private real estate loans, Hard money loans, Private real estate mortgage, Hard money mortgage lender, Hard money mortgage lender, residential hard money loans, commercial hard money loans, private mortgage lender Hard Money Lender, Private lender